Soybean futures sank to the lowest levels in over a week while corn futures traded on both sides of unchanged before ending with modest gains as traders shrugged off a few bullish numbers in today’s USDA Supply and Demand update and focused on favorable growing conditions and an outlook for strong U.S. harvests.

Today’s report carried some reasons for longer-term optimism for the corn market as USDA said it expected next year’s global supplies to be even tighter than the agency initially projected a month ago. USDA also hiked its estimate for U.S. corn exports during the current crop year by almost 2%, an acknowledgement of demand that’s remained strong late into the marketing year.

USDA data was more of a mixed bag for soybeans and wheat. U.S. wheat exports in 2025-26 were revised higher but winter wheat production came in higher than expected.

Today’s market reaction indicates traders are more focused on U.S.-China trade developments and Midwest weather, which has been largely favorable for early crop development.

July corn futures rose 1.5 cents to $4.3850 per bushel, while December corn rose 0.75 cent to $4.4050. July soybeans fell 8.25 cents to $10.4225, while November soybeans fell 2 cents to $10.2725, the contract’s lowest close since June 4. July SRW wheat futures fell 7.75 cents to $5.2650, near a four-week low.

The following are brief summaries from today’s USDA Supply and Demand and Crop Production reports:

Corn supply outlook shrinks further

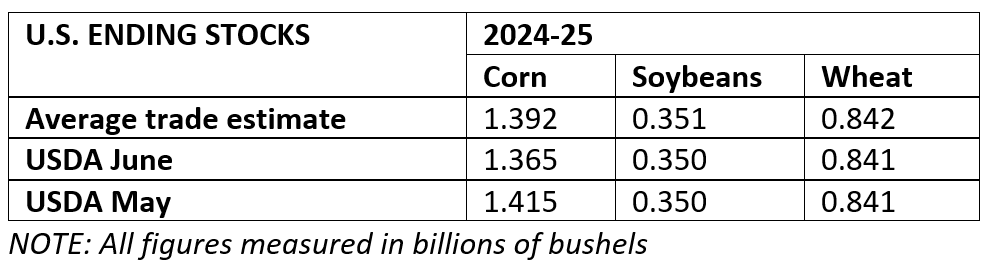

USDA lowered its estimates for U.S. corn stockpiles at the end of the 2024-25 and 2025-26 marketing years and also hiked its forecast for 2024-25 U.S. corn exports by 50 million bushels, to 2.65 billion bushels, up 16% from 2023-24 and the second-highest on record.

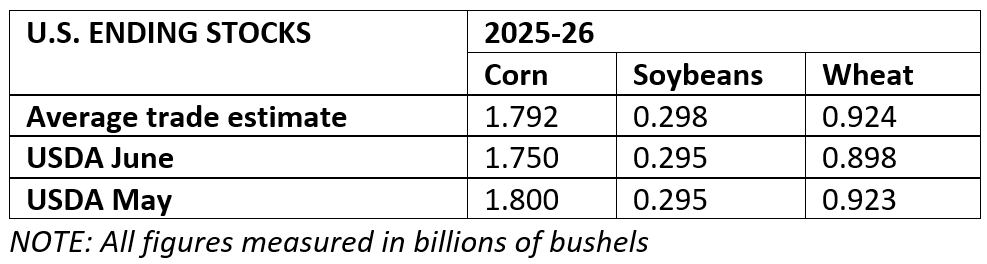

Ending stocks for 2024-25 were lowered 50 million bushels to 1.365 billion bushels, a drop of nearly 23% from 2023-24. Stocks are seen at 1.75 billion bushels at the close of 2025-26, also down 50 million bushels from last month’s estimate.

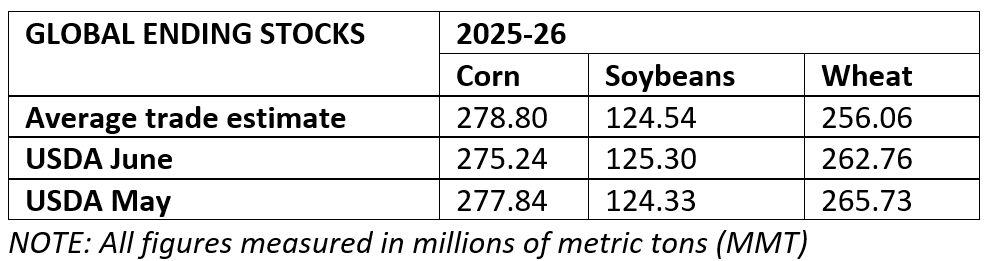

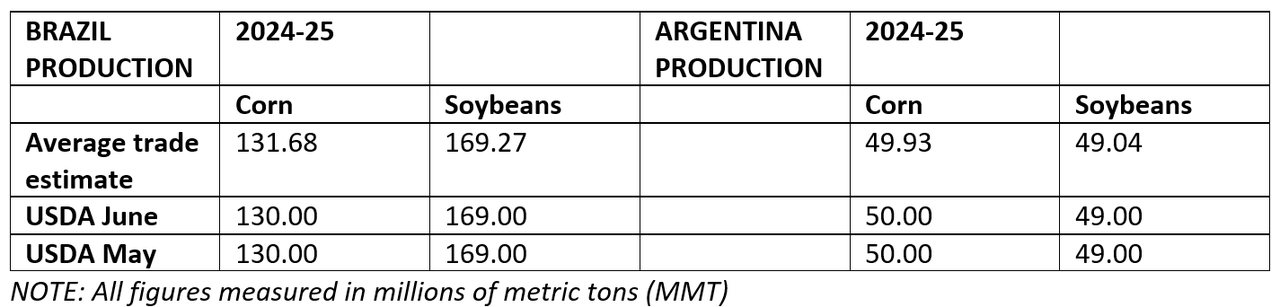

Among global figures, USDA cut its forecast for 2025-26 ending stocks by 0.9% to at 275.24 million metric tons (10.8 billion bushels), which would be down 3.4% from 2024-25 and the lowest since 2013-14. Argentina’s and Brazil’s 2025 corn crops were left unchanged at 50 MMT and 130 MMT, respectively.

In March, USDA forecast U.S. corn plantings at 95.3 million acres, up 5.2% from 2024 and the highest since 2013. USDA will release updated survey-based acreage figures on June 30.

Also today, USDA kept its projected average U.S. farm price for corn in 2025-26 unchanged at $4.20, down from $4.35 in 2024-25.

Soybean supplies seen expanding in 2026

USDA left soybean stocks at the end of 2024-25 and 2025-26 unchanged at 350 million bushels and 295 million bushels, respectively, contrary to analysts’ expectations for a small increase in the latter figure.

U.S. soybean exports for 2024-25 and 2025-26 were held unchanged at 1.85 billion bushels and 1.815 billion bushels, respectively. USDA also kept its Argentina and Brazil production forecasts unchanged at 49 MMT and 169 MMT, respectively (1.8 billion bushels and 6.21 billion bushels).

Global stockpiles are seen expanding further next year amid expectations for even larger crops in South America.

USDA hiked estimated global soybean supplies at the end of 2025-26 by 0.8% from last month’s figure to 125.3 MMT (4.6 billion bushels), up 0.8% from 2024-25 and a record amount. Brazil’s 2026 crop was pegged at 175 MMT, unchanged from last month. Argentina’s crop was estimated at 48.5 MMT.

Farm-level soybeans are expected to average $10.25 in 2025-26, up from $9.95 in 2024-25. Both estimates were unchanged from USDA’s May report.

Wheat

The Supply and Demand report carried some price-supportive numbers for wheat, as USDA left expected 2024-25 ending stocks unchanged at 841 million bushels but cut its 2025-26 estimate by 25 million bushels to 898 million bushels.

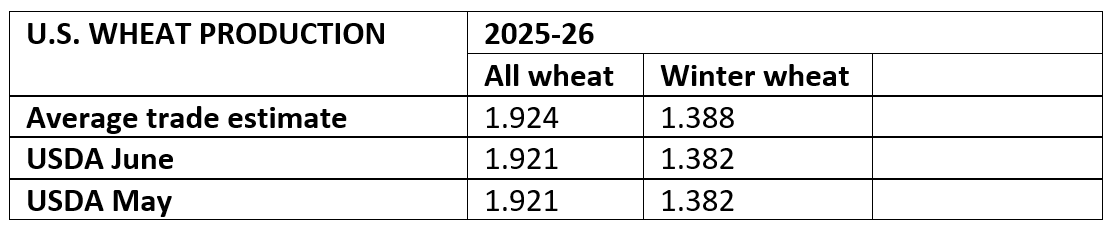

U.S. production of all varieties of wheat in 2025-26 was lowered 50 million bushels to 1.921 billion bushels, down 2.5% from 2024-25. Winter wheat production was left unchanged at 1.382 billion bushels, contrary to expectations for a slight increase but still a nine-year high.

Global supplies in 2026 are expected to be smaller than previously forecast. USDA cut its forecast for 2025-26 ending wheat stocks by 1.1% to 262.76 MMT (9.65 billion bushels), down 0.5% from 2024-25 and a 10-year low.

The average farm price for wheat in 2025-26 was raised 10 cents to $5.40 per bushel, down from $5.50 in 2024-25.

The following is a brief summary of key figures from today’s USDA Supply and Demand report: